How to reduce EFTPOS fees and payment costs in your retail business

Running a retail business is hard enough without watching a chunk of your profits disappear into EFTPOS fees. With more customers paying by card than ever before, payment costs have become one of the biggest ongoing expenses for shop owners. The problem is, many retailers don’t realise just how much these fees are costing them — or what they can do to bring them down.

I’ve spent time with retailers who thought EFTPOS costs were just part of doing business, only to discover they could save thousands of dollars each year with a few smart changes. In this post, I’ll walk through what EFTPOS fees are, why small retailers often overpay, and the strategies you can use to cut payment costs without cutting service.

Understanding EFTPOS fees in Australia

Before you can reduce fees, you need to know what you’re paying for. EFTPOS costs come from several different charges:

- Terminal rental: the cost of leasing or buying your card machine.

- Merchant service fees: a percentage of each transaction, often 0.5%–2%, depending on the card type and provider.

- Interchange and scheme fees: charged by Visa, Mastercard, or American Express, usually passed through by your bank or provider.

- Other charges: settlement fees, minimum monthly charges, chargeback costs, or even early termination fees if you switch providers.

Some providers offer flat-rate pricing, where you pay one fee per transaction regardless of the card. Others use blended or interchange-plus pricing, where the cost varies depending on whether the customer uses a debit, credit, or premium card.

For a retailer processing $50,000 a month, even a 0.3% difference in fees can add up to $150 a month, or $1,800 a year. That’s money that could go towards wages, rent, or stock.

Why small retailers often overpay

I’ve noticed that small retailers tend to overpay for one simple reason: they don’t review their payment setup often enough.

Here are some common reasons:

- Lack of transparency: Many banks bundle EFTPOS with business accounts but don’t break down the true cost.

- Outdated plans: Retailers stick with legacy pricing from years ago, even though more competitive options now exist.

- Low transaction volumes: Smaller businesses often don’t push for better rates because they assume they have no leverage.

- Not shopping around: Fintech players like Tyro, Square, and Zeller often undercut the big banks, but many retailers don’t compare.

The good news is, once you know what to look for, you can take control.

How to cut EFTPOS costs

Reducing EFTPOS fees doesn’t have to be complicated. Here are the most effective strategies I’ve seen retailers use.

1. Negotiate with your provider

Banks and payment companies rarely offer their best rate up front. If you’ve been with the same provider for more than two years, call them and ask for a review. Use your turnover figures as leverage. If you process $250,000 a year, you should not be paying the same rates as a retailer processing $50,000.

Don’t be afraid to mention competitor offers. Providers know how easy it is to switch these days, and they’d rather keep your business than lose you over a small fee difference.

2. Compare different providers

Traditional banks no longer have a monopoly on EFTPOS. New fintech providers often offer flat-rate pricing, no hidden fees, and faster settlement times. For example, Square charges a transparent percentage per transaction with no terminal rental. Tyro offers competitive rates and integrates with many POS systems.

Even if you don’t switch, getting a quote gives you bargaining power with your current provider.

3. Use least-cost routing

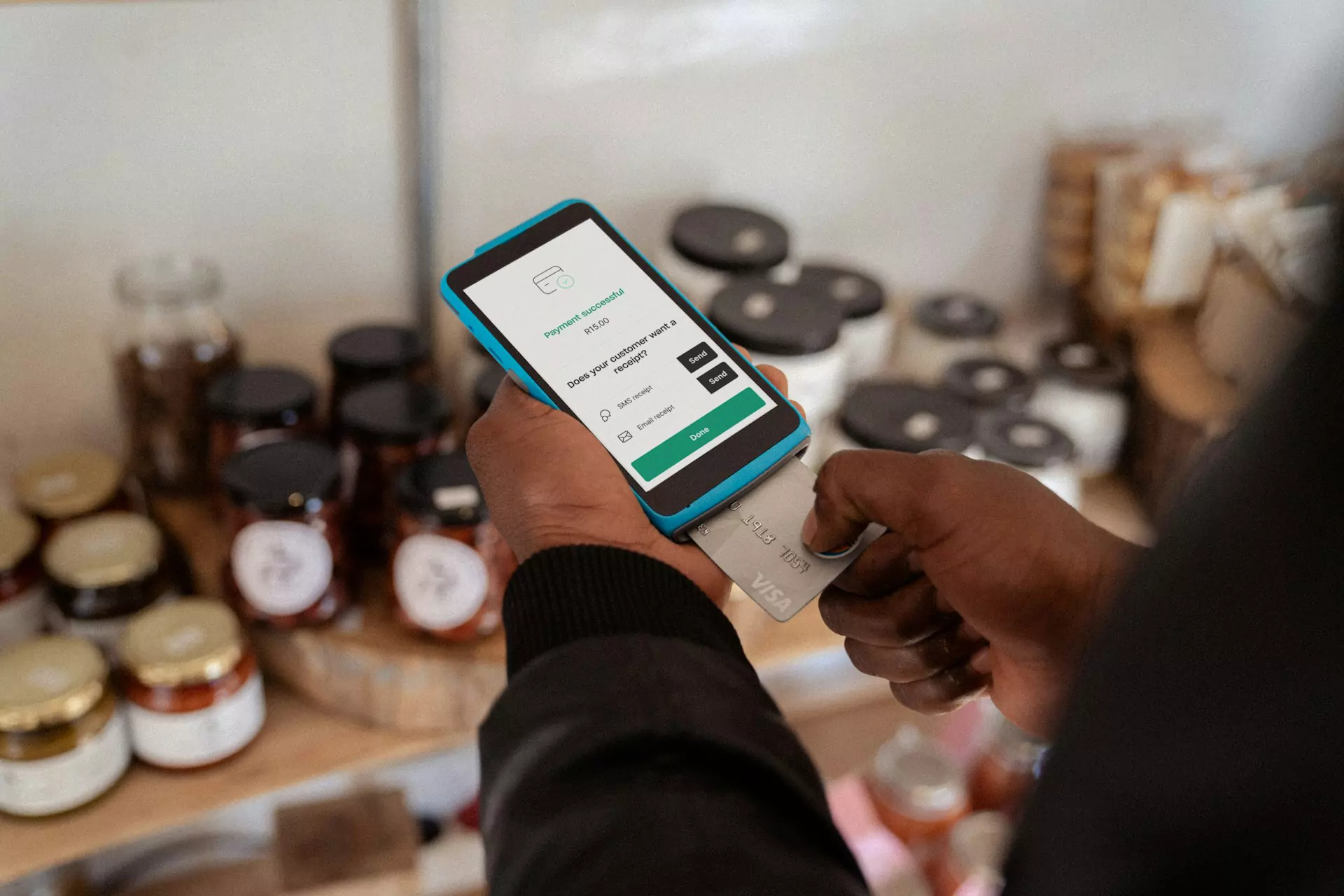

One of the most overlooked ways to save is least-cost routing. When a customer taps their card, the transaction can be processed through either the domestic EFTPOS network or the international card schemes (Visa or Mastercard). By default, many terminals route through the more expensive scheme rails.

Least-cost routing automatically chooses the cheaper option, usually EFTPOS debit for local cards. This can save retailers thousands a year, especially if most of your customers pay with debit. Ask your provider if your terminal supports it — if not, consider upgrading.

4. Review your terminal costs

Some providers charge high rental fees for terminals, often $30–$50 per month. Over three years, that’s over $1,000. In many cases, it’s cheaper to buy a terminal outright or use a mobile solution like Tyro or Zeller, which only charge transaction fees.

If you operate multiple locations, look at whether you really need a terminal on every counter. Mobile terminals can often be shared, reducing rental costs.

5. Encourage lower-cost payment methods

While you can’t stop customers from paying with premium credit cards, you can nudge them towards cheaper options. For higher-value transactions, offer incentives for direct debit or bank transfer. For regular customers, set up standing orders or recurring payments.

You can also add a surcharge to cover the cost of expensive card payments. For example, charging 1.5% for American Express while keeping debit card payments free. Just make sure you follow the compliance rules.

Optimising your payment mix

Not all payments are created equal. A key step in reducing costs is understanding what types of cards your customers use.

- Debit cards: usually the cheapest to process, especially via EFTPOS.

- Credit cards: cost more, particularly premium and rewards cards.

- International cards: often the most expensive.

By analysing your transaction data, you can see the percentage split and make informed decisions. For example, if 70% of your transactions are debit, enabling least-cost routing could deliver major savings.

Surcharging and compliance

In Australia, businesses can legally pass on card surcharges, but only up to the cost of acceptance. The ACCC enforces this, and fines apply if you overcharge.

That means if your average merchant fee is 1.2%, you can apply a 1.2% surcharge — but not 2% or more. Some terminals automatically calculate surcharges based on your actual rates, which makes compliance simple.

When applied transparently, surcharging can protect your margins while still giving customers choice. For example, a clothing store might offer free EFTPOS for debit but add a 1.5% surcharge for premium credit cards. Most customers accept this when it’s explained clearly.

Reduce admin costs with automation

EFTPOS fees aren’t just about percentages. The time you spend reconciling payments and calculating costs is also a hidden expense.

I’ve seen retailers spend hours each week manually matching EFTPOS settlements against bank deposits. With an automated accounting tool like Thriday, that process takes seconds. Transactions are reconciled automatically, fees are categorised correctly, and you get real-time reporting on payment costs.

This visibility helps you see whether your strategies are working — and frees up more of your time to run your business.

When paying more makes sense

It’s tempting to chase the lowest possible rate, but sometimes paying slightly more delivers better value. For example:

- Faster settlement: Same-day funds can improve cash flow, even if fees are slightly higher.

- Integrated POS features: Terminals that link seamlessly with your till reduce admin and errors.

- Added services: Health claiming, loyalty integration, or multi-currency acceptance may justify higher costs if they bring in more customers.

The goal isn’t to pay the least, but to pay the right amount for the value you receive.

Final thoughts

EFTPOS fees might feel like a fixed cost of doing business, but they’re not. By negotiating with providers, enabling least-cost routing, reviewing terminal costs, and using automation, you can protect your margins and put more money back into your retail business.

Even small savings add up quickly when you process hundreds of transactions a day. The key is to stay proactive — review your setup regularly, compare alternatives, and use the tools available to stay on top of costs.

With the right approach, you’ll stop payment fees eating away at your hard-earned profits and keep your business financially healthy.

DISCLAIMER: Team Thrive Pty Ltd ABN 15 637 676 496 (Thriday) is an authorised representative (No.1297601) of Regional Australia Bank ABN 21 087 650 360 AFSL 241167 (Regional Australia Bank). Regional Australia Bank is the issuer of the transaction account and debit card available through Thriday. Any information provided by Thriday is general in nature and does not take into account your personal situation. You should consider whether Thriday is appropriate for you. Team Thrive No 2 Pty Ltd ABN 26 677 263 606 (Thriday Accounting) is a Registered Tax Agent (No.26262416).

.svg)

.webp)